Reflections from the Finance in Common Summit.

Published on: 24/11/2022

The involvement of African Development Banks in water and sanitation finance remains limited.

“You cannot industrialise with a double-digit interest rate” – commented a gentleman from the National Bank of Nigeria at the third edition of the Finance in Common Summit, co-hosted by the European Investment Bank and the African Development Bank on the 18th of October in Abidjan. He was referring to the high costs of capital available to public finance institutions to be able to on-lend. Private finance institutions use even higher rates.

Unlike other conferences, the Summit had a very strong research basis and provided a useful moment to reflect on the role of Public Development Banks (PDBs), specifically in Africa. Given that globally PDBs can provide cheaper single-digit interest rates to socially relevant sectors, why are PDBs in African countries invisible when it comes to investments in the WASH sector? While there was not much sector-specific information provided during the summit there were, nevertheless, some useful insights for the WASH sector from different pieces of research.

The database on Public Development Banks keeps growing and more details are added every year. Currently (in 2022), the database captures 522 PDBs in 154 countries managing US$ 23.21 trillion of assets. Two facts stood out:

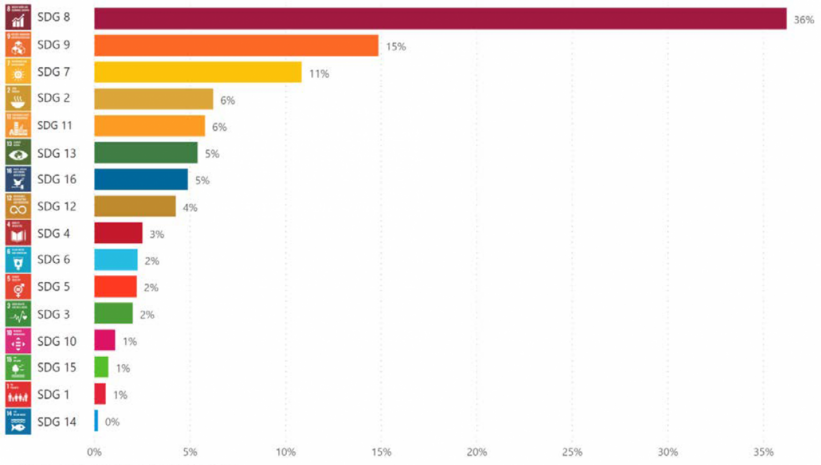

One study used artificial intelligence to check the alignment of 237 PDBs with the 2030 SDG Agenda over a 5-year period (between 2016-2020). It concluded that the majority of the PDBs invest in the “productive SDGs” – especially those that support ecosystems of small and medium enterprises (SMEs) and/or directly benefit economic development. Put another way, PDBs invest in sectors that are seen as being able to pay back loans:

As can be seen in the figure below, a very low percentage of PDBs invest in SDG 6 (universal access to clean water and sanitation services). Zooming in on the African Region, SDG 2 (food security) and SDG 1 (end poverty) have a higher priority among the PDB investments.

Share of Sustainable Development Goal narrative in annual reports. Source: AFD.

The European Investment Bank (EIB) undertook a survey of African banks in 2022, both public and private. The major difficulties of the banks in Africa are related to increasing costs of capital and the depreciation of their currency, both of which make it hard for them to access cheaper capital.

During COVID, the portfolios of African banks remained resilient as central banks and regulators responded by lowering requirements for liquidity and risk management. However, the bulk of additional capital was raised from a combination of African and international commercial bank loans and increased deposits, not from public budgets.

Looking at climate finance, in Africa there is an increase in banks that do climate screening, lending, and funding and the trend is here to stay. However, technical capacity was cited as a barrier to identifying climate risks and opportunities by 60% of banks; and 67% of the banks surveyed think International Finance Institutions can support them in expanding green lending – primarily through training and technical assistance.

From a gender perspective, 70% of the banks surveyed have a gender strategy in place and 59% offer financial services that are targeted at women. Even more interesting, more than 40% of banks see lower non-performing loans (NPL rations) on female loans.

Even although the Finance in Common Summit did not talk much about water, it gave us the latest insights into the challenges facing PDBs in African countries. It does reinforce much of what we already know about the sorts of reform needed in the sector.

Against this background, the opportunities for the water and sanitation sector are clearly in the development of projects that align water and sanitation goals with climate resilience and mitigation, projects aiming to increase food security, SMEs and women. But they also require creditworthy service providers and SMEs that can pay back loans, and probably, a set of guarantees to get the national PDBs to engage comfortably with the sector.

These and other recommendations and case studies specifically for the water sector can be accessed in the global study done in 2021 on the role of National Public Development Banks in financing the water and sanitation SDG 6, available here.

The research papers presented at the Summit can be found here.

The recorded videos and presentations from the Finance in Common Summit can be found here.

At IRC we have strong opinions and we value honest and frank discussion, so you won't be surprised to hear that not all the opinions on this site represent our official policy.